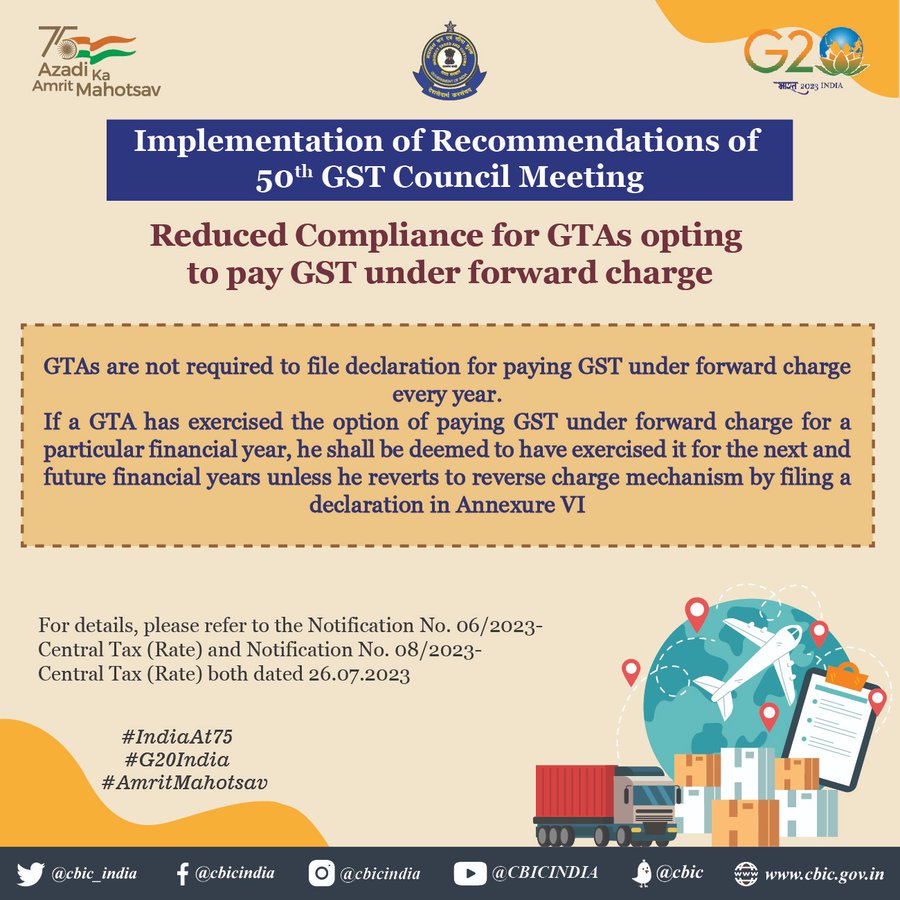

CBIC has made amendments to its previous Notifications to implement changes recommended by the GST Council. These changes pertain to Goods Transport Agencies (GTAs) and their choice of tax payment mechanism, either Forward Charge Mechanism (FCM) or Reverse Charge Mechanism (RCM).

GTAs now have the freedom to choose between FCM and RCM during the period from 1st January to 31st March of the preceding Financial Year. The deadline for making this choice has been extended to 31st March instead of the earlier date of 15th March.

GTAs are no longer required to submit Annexure V every year to opt for FCM. They only need to file this declaration once unless they wish to switch to RCM.

If GTAs choose to pay tax under FCM by filing Annexure-V, it will be considered as their choice for all future years unless they decide to switch to RCM. To switch to RCM, they need to file a declaration in Annexure VI.

Once the GTA opts for RCM through Annexure VI, it will be considered as their choice for all future years unless they decide to switch back to FCM.

Amendments to Central Tax Notifictaion 11/2017:

CBIC Central Tax Rate Notification 6/2023 dated 26/07/2023: Choosing FCM or RCM Options Simplified for GTAs

CBIC Integrated Tax Rate Notification 6/2023 dated 26/07/2023: Choosing FCM or RCM Options Simplified for GTAs

CBIC UT Tax Rate Notification 6/2023 dated 26/07/2023: Choosing FCM or RCM Options Simplified for GTAs

Amendments to Central Tax Notifictaion 13/2017:

CBIC Central Tax Rate Notification 8/2023 dated 26/07/2023: Exemption from Annual Declaration by GTAs on Choosing FCM or RCM Option

CBIC Integrated Tax Rate Notification 8/2023 dated 26/07/2023: Exemption from Annual Declaration by GTAs on Choosing FCM or RCM Option

CBIC UT Tax Rate Notification 8/2023 dated 26/07/2023: Exemption from Annual Declaration by GTAs on Choosing FCM or RCM Option